Every quarter, The GEAR convenes its Startup CoLab programme partners for a closed-door partner forum, which is part programme review, part market signal scan, and part working session on where the built environment is actually moving. The forum is anchored by a standing group of six founding programme partners: JTC, BCA, ACE.SG, Enterprise Singapore, HKSTP, and SMU IIE.

The value of these forums is structural. Between The GEAR and our programme partners, we collectively see a cross-section of built environment startups across geographies, stages, and problem sets. Patterns, therefore, emerge early, and often even before they are visible at the market level. What shows up first in the startup pipeline tends to signal where the industry is going, not just where it currently is.

Several themes stood out from our Q1 2026 discussion.

Embodied carbon is moving from compliance to core strategy

For the past decade, embodied carbon in construction has largely been a measurement problem: how to calculate it, report it, and comply with evolving standards. A growing share of the founders we’re meeting are no longer building tools to measure carbon. They’re building the materials that reduce it. We’re seeing:

Lifecycle carbon platforms that automate calculation across the project’s full scope

Additives that materially improve the performance of low-carbon concrete

Cement-free structural materials derived from waste streams and industrial by-products

Biomaterial alternatives for interior systems and finishes

The distinction matters. While measurement tools make the problem visible, material innovation moves the number. The most ambitious founders in this space have understood the difference and are building accordingly.

For contractors and developers, the implication is straightforward. Carbon reduction will not come from better dashboards. It will come from earlier materials decisions and a supply chain that is starting to offer credible alternatives.

AI is becoming a unifying layer, not a replacement

The second shift is about how AI is being deployed. The strongest AI startups we are seeing are not replacing existing tools. They are building on top of them. We are seeing:

Low-code connectors into platforms teams already use

Risk signals surfaced from contracts and schedules

Drawing and BIM analysis

On-demand dashboards in plain English

Unified search across fragmented project data

This pattern suggests that the value is not building the next system. It is in making existing systems work as one. This reflects what we are seeing internally. The appetite for new technology is high, but tolerance for disruption is low. Tools that require a full overhaul rarely move beyond pilots. Tools that fit into existing workflows are far more likely to be adopted.

In this context, the winners will not replace the stack. They will unify it.

The Q1 pipeline in numbers

The qualitative trends are reflected in the pipeline. A snapshot of the startups assessed in Q1 2026 shows where the market is today.

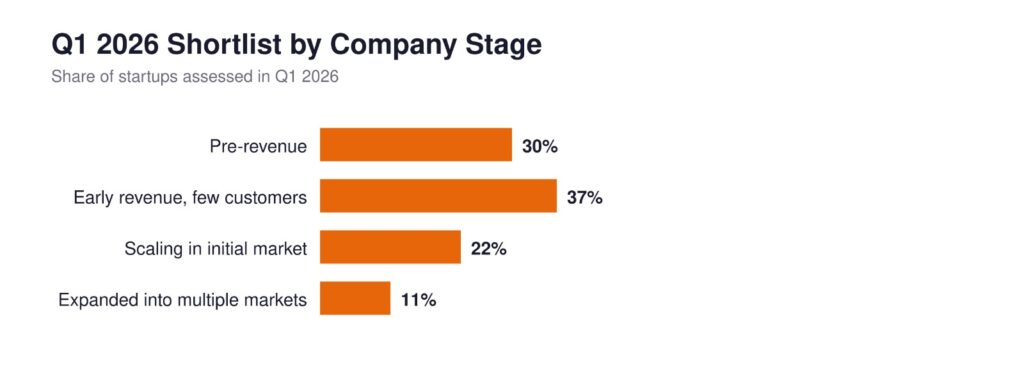

The pipeline is overwhelmingly early-stage. Most startups are pre-revenue or in the earliest stages of traction, with limited geographic expansion. More than half have raised under $1 million. Nearly a quarter are fully bootstrapped. This is the stage where access to a tier-one contractor, a live deployment environment, and a structured proof-of-concept can materially change trajectory.

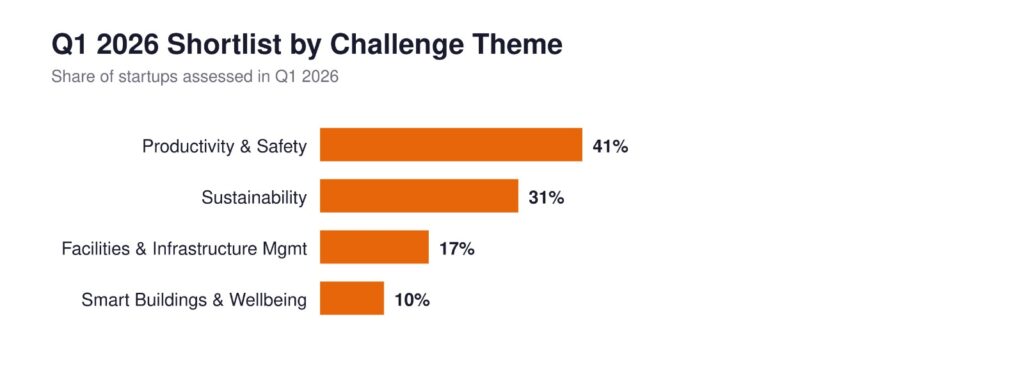

Two themes dominate the pipeline. Productivity, safety, and sustainability account for the majority of the shortlist, reflecting where ConTech investment has been concentrated in recent years. In contrast, smart buildings, occupant wellbeing, and facilities management remain underrepresented relative to the size of the opportunity.

The pipeline is global. Most of the startups shortlisted this quarter are headquartered outside Singapore, spanning Asia, Europe, North America, and Oceania. This reflects a deliberate channel strategy built with ecosystem partners in markets we do not reach directly, and gives the programme visibility into innovation beyond a Singapore vantage point.

What this tells us about the year ahead

The signal is consistent. Innovation in the built environment is moving away from surface-level optimisation and toward solutions that are either deeper or more embedded. In materials, that means changing the underlying inputs. In AI, it means integrating into existing workflows.

And increasingly, it is early-stage founders who are solving for the hardest constraint: adoption.

That is the lens we will carry into the rest of 2026, both in how we select the next intake of Startup CoLab and how we work with our programme partners to bring promising startups into real-world deployment.

End of the article.